On Saturday night SBA issued a “reminder” regarding their ability to review PPP loans. SBA’s interim final rule on SBA Loan Review Procedures and Related Borrower and Lender Responsibilities indicates that SBA may review any PPP loan, of any size, at any time. While it is unclear what might cause a loan review on a loan of less than $2 million, it appears as though SBA is using the same edit checks configured for PPP 2.0 to validate eligibility and loan amounts for PPP loans received in 2020. One of the issues we are seeing is errors in the loan amount on the First Draw loans that are impacting approvals on Second Draw loans. If you have applied for forgiveness on your First Draw loan, your lender has the ability to escalate that review process through the SBA Forgiveness Platform. Once the discrepancy is resolved, the Second Draw loan can be reviewed for approval.

According to the SBAs procedural notice, loan amounts may be deemed incorrect either because they do not properly exclude individual employee salary costs exceeding $100,000 or because the borrower included costs paid to independent contractors that did not constitute “payroll costs”. Independent contractors are eligible to apply for PPP loans on their own.

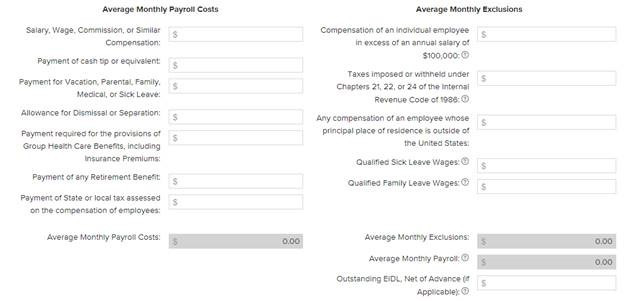

If you have a single employee, the math is easy. You can count up to $100,000 in salary and wages for the employee. Prorated for 2.5 months, that dollar amount is $20,833, plus the cost of benefits. Owner compensation is capped at $20,833 because it already contemplates the cost of employer contributions for group health, life, disability, vision, and dental insurance. According to the SBA’s FAQs, “In addition to [the specific caps for individual employees], payroll costs for determining loan amount for owner-employees and self-employed individuals’ payroll compensation is capped at $20,833 per individual.”

For businesses in the Accommodation and Food Services sectors with a NAICS code of 72, prorated for 3.5 months, the SBA caps wages at $30,000 per employee as one of the edit checks for approving a Second Draw loan. SBA recognized that the “adjustment for maximum loan amount and employee guidance” was one of the top issues they are hearing about from bankers, and has since made adjustments to increase the validation rule it had in place from $30,000 to $35,000 per employee. This means that the total loan requested cannot exceed the number of employees multiplied by $35,000. It’s being increased in acknowledgment of factors other than the salary limit of $100,000, such as benefits. This remains a validation rule and is not intended to set the appropriate maximum based on other criteria such as NAICS codes that do not begin with 72. As before, restrictions on owner compensation apply. Refer to SBA’s guidance on calculating Second Draw Loan Amounts for additional details based on each entity type.

If you have not yet applied for forgiveness, and your First Draw PPP Loan is under review by the SBA and/or a determination has been made that you are ineligible for a PPP loan, the SBA may also send a notification to your PPP lender that you are an “unresolved borrower” at the time your Second Draw loan is submitted for approval. As per the FAQs issued on Second Draw loans, the SBA will not issue an SBA loan number, and additional loans are prohibited from being made until the outstanding issues are resolved. The FAQs state that SBA will “resolve issues related to unresolved borrowers expeditiously,” but it still could result in a delay in the approval and funding of Second Draw PPP loans for these borrowers.

SBA further clarified in their PPP Program Update issued Saturday evening that if a borrower’s First Draw PPP Loan is under review by SBA for any reason, including if information in SBA’s possession indicates that the borrower may have been ineligible for the First Draw PPP Loan it received or for the loan amount it received, the lender will receive notification from SBA when the lender submits an application for a Second Draw PPP Loan, and will not receive an SBA loan number until the issue related to the unresolved borrower’s First Draw PPP Loan is resolved.

While no one knows how long the funds will be available, it appears as though the money will last longer than it did during the first appropriation of funds in 2020 due to the new approval process described above, combined with the “pacing” of applications, which began by limiting access to the PPP loan portal to Community Financial Institutions, followed closely by allowing access to community banks and credit unions with less than $1 billion in assets on Friday, January 15, 2021. SBA issued a press release after the first week of the program, noting that they had approved approximately 60,000 PPP loan applications submitted by nearly 3,000 lenders, for over $5 billion, between the program’s re-opening on Monday, Jan. 11, at 9 a.m. ET through to Sunday, Jan. 17. With $284 billion total funds available, there were significant funds still remaining when the portal opened to all other lenders early the morning of January 19, 2021.

Thanks for reading! We will continue to bring you the latest as we receive it. Be sure to check our PPP page regularly for updates and answers to frequently asked questions!

Previous: Guidance on Second Draw PPP Next: PPP Loans