SBA issued Interim Final Rules on Wednesday, January 6, 2021 to renew the Paycheck Protection Program (PPP) as required by the new Economic Aid to Hard-Hit Small Businesses, Non-Profits, and Venues Act (Economic Aid Act). We don’t yet know when the SBA application portal will reopen for financial institutions, but likely by mid-January. We also don’t yet know when the revised PPP loan application will be made available by SBA; however, we understand it could be within the next 48 hours.

We expect additional rules to implement other provisions of the Economic Relief Act, including clarification for new expenses eligible for forgiveness and procedures for returning EIDL advances deducted from loans to borrowers who received forgiveness before December 27, 2020. Already, calculations for the forgiveness amount on any forgiveness applications submitted on or after December 28, 2020 no longer include a deduction for EIDL advances received by the business.

You can refer to our PPP page of our website for additional updates as we receive them, as well as our FAQs for both the forgiveness process and the PPP2 application process. In addition, we are providing a brief overview of some common questions in this blog post.

We do not yet know; however, the Interim Final Rules indicate they are effective “immediately”. In addition, SBA issued a statement committing to promote awareness of their policies and procedures via traditional media methods, SBA social media accounts and guidance to lenders before the formal opening of SBA’s loan systems. We do know the last day to apply for, and receive, a PPP loan is March 31, 2021. We also understand that, on Monday, January 11, 2021, the portal will reopen for “community financial institutions,” which include community development financial institutions, minority depository institutions, certified development corporations and microloan intermediaries making first-draw PPP loans. On Wednesday, these community financial institutions may begin making second-draw PPP loans, and the program will open to all remaining lenders “shortly thereafter,” likely the following week. We anticipate we will begin sending customized links to ARB clients who have submitted expressions of interest to begin their applications early next week.

Read the full SBA press release

In reality, not much has changed for businesses applying for their first PPP loan. The Consolidated First Draw PPP Interim Final Rule, reminds borrowers that SBA’s affiliation rules (13 CFR 121.301) do not apply to any business entity that is assigned a NAICS code beginning with 72 (Hospitality or food service industry) and that employs not more than a total of 500 employees. This means that if each hotel or restaurant location owned by a parent business is a separate legal business entity and employs not more than 500 employees, each hotel or restaurant location is permitted to apply for a separate PPP loan provided it uses its unique EIN.

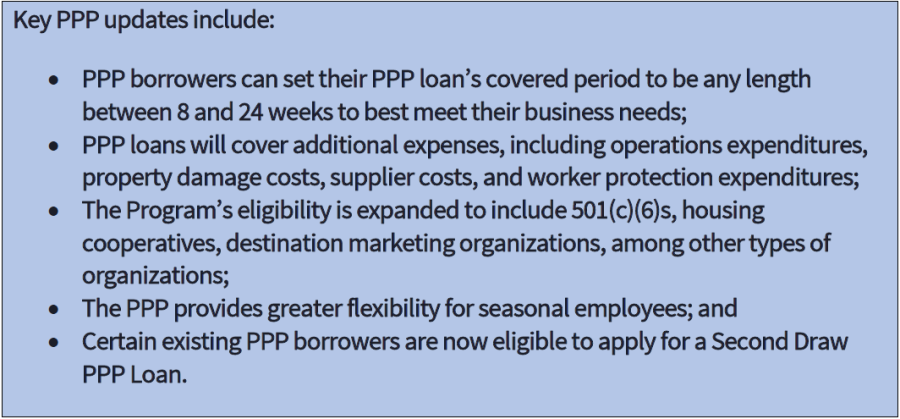

There have been a few changes to eligible businesses, to include certain newspaper outlets and 501(c)6 organizations that were previously excluded under the original PPP loan program, but for the most part the original PPP definition for eligible businesses is the same. Publicly traded companies, companies receiving passive income, and those participating in federally illegal activities continue to be ineligible for PPP loans.

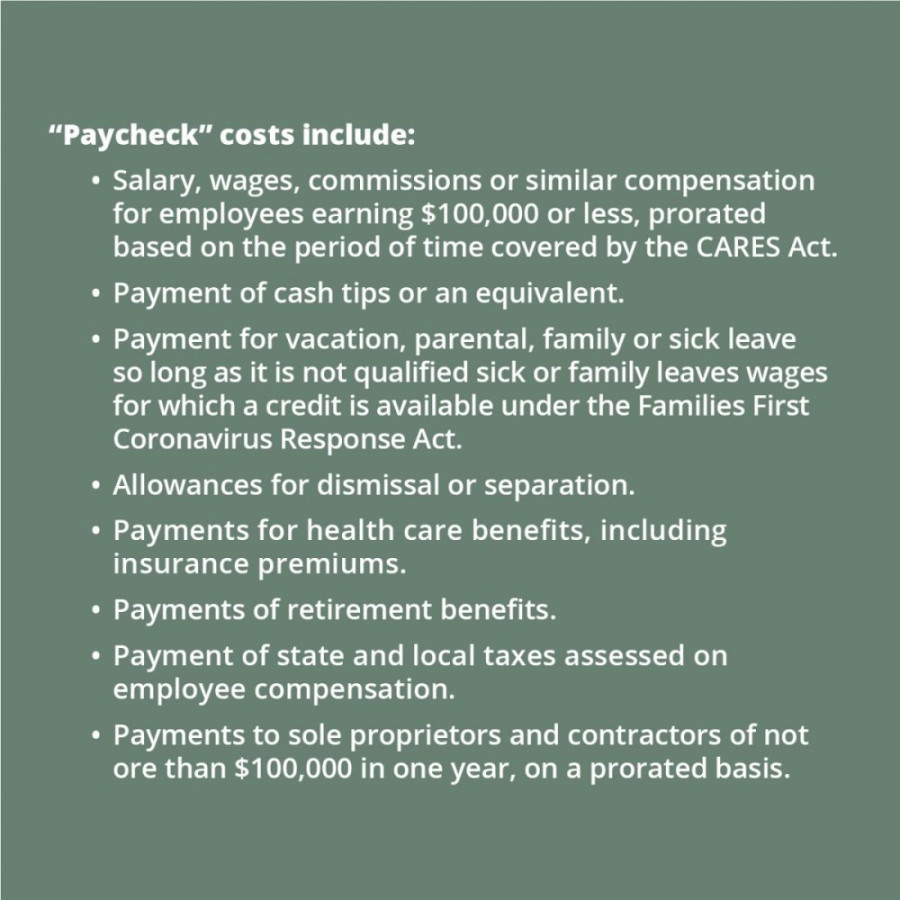

Of note is the fact that the Economic Aid Act required payroll costs to be based upon payroll costs incurred during the 1-year period before the date on which the loan is made. For PPP loans made in 2020, most borrowers used 2019. The First Draw IFR makes it clear that new borrowers can choose either 2019 or 2020 as their base period for calculating payroll costs, thereby ensuring that they are able to obtain funding consistent with existing PPP borrowers.

You must submit documentation sufficient to establish eligibility and to demonstrate the qualifying payroll amount, which may include, as applicable, payroll records, payroll tax filings, Form 1099-MISC, Schedule C or F, income and expenses from a sole proprietorship, or bank records.

Yes! Businesses “still in operation” are eligible for a second draw loan in accordance with the program requirements outlined in the IFR for Second Draw Loans up to a maximum loan amount of $2 million. In general, the Economic Aid Act made the eligibility requirements for Second Draw PPP Loans narrower than the eligibility requirements for First Draw PPP Loans. The Economic Aid Act generally provides that a borrower is eligible for a Second Draw PPP Loan only if it:

To assist those businesses that don’t maintain quarterly filings, the IFR also provides that a borrower that was in operation in all four quarters of 2019 is deemed to have experienced the required revenue reduction if it experienced a reduction in annual receipts of 25 percent or greater in 2020 compared to 2019 and the borrower submits copies of its annual tax forms substantiating the revenue decline. This provision will allow a borrower to provide annual tax return forms to substantiate its revenue reduction.

The IFR defines “gross receipts” consistent with the definition of receipts in 13 C.F.R. 121.104 of SBA’s size regulations:

“all revenue in whatever form received or accrued (in accordance with the entity’s accounting method) from whatever source, including from the sales of products or services, interest, dividends, rents, royalties, fees, or commissions, reduced by returns and allowances. Generally, receipts are considered “total income” (or in the case of a sole proprietorship, independent contractor, or self-employed individual “gross income”) plus “cost of goods sold,” and excludes net capital gains or losses as these terms are defined and reported on IRS tax return forms. Gross receipts do not include the following: taxes collected for and remitted to a taxing authority if included in gross or total income (such as sales or other taxes collected from customers and excluding taxes levied on the concern or its employees); proceeds from transactions between a concern and its domestic or foreign affiliates; and amounts collected for another by a travel agent, real estate agent, advertising agent, conference management service provider, freight forwarder or customs broker. All other items, such as subcontractor costs, reimbursements for purchases a contractor makes at a customer's request, investment income, and employee-based costs such as payroll taxes, may not be excluded from gross receipts.”

Proceeds from first round PPP program are not included in gross receipts.

As with first time PPP loans, there is a special affiliation exemption for restaurants and hotels for second PPP loans. However, business concerns with a NAICS code beginning with 72 only qualify for the affiliation waiver for Second Draw PPP Loans if they employ 300 or fewer employees. Eligible news organizations with a NAICS code beginning with 511110 or 5151 (or majority-owned or controlled by a business concern with those NAICS codes) may qualify for the affiliation waiver for Second Draw PPP Loans only if they employ 300 or fewer employees per physical location. However, subsection (f)(9) provides that businesses that are part of a single corporate group shall in no event receive more than $4,000,000 of Second Draw PPP Loans in the aggregate.

In general, the IFR provides that the maximum loan amount for a Second Draw PPP Loan is equal to the lesser of two and half months of the borrower’s average monthly payroll costs or $2 million, based upon payroll costs calculated using either the calendar year 2020 or the calendar year 2019. However, the rule notes that Second Draw PPP Loan borrowers who are not self-employed (including sole proprietorships and independent contractors) are also permitted to use the precise 1-year period before the date on which the loan is made to calculate payroll costs if they choose not to use 2019 or 2020 to calculate payroll costs. There are a few modifications to this maximum loan amount calculation, including for seasonal businesses, farmers and ranchers, and new entities that did not exist for the full twelve-month period preceding the Second Draw PPP Loan.

In addition, for borrowers assigned a NAICS code beginning with 72 at the time of disbursement, the Economic Aid Act provides that the maximum loan amount is equal to three-and-a-half (3.5) months of payroll costs rather than two-and-a-half (2.5) months.

You may use either 2020 or 2019 data to calculate your Second Draw Loan; however, we will not require additional documentation to substantiate payroll costs if you:

The IFR provides that lenders may request additional documentation to conduct a review of eligibility. In addition, for loans with a principal amount greater than $150,000, you must also submit documentation adequate to establish that you experienced a revenue reduction of 25% or greater in 2020 relative to 2019 as defined above. Such documentation may include relevant tax forms, including annual tax forms, or, if relevant tax forms are not available, quarterly financial statements or bank statements. For loans with a principal amount of $150,000 or less, such documentation is not required at the time you submit your application for a loan, but it must then be submitted on or before the date you apply for loan forgiveness, or at the request of SBA if you haven’t applied for forgiveness.

The original definition for determining the maximum loan amount has not changed, although the definition of eligible expenses for forgiveness has been expanded slightly under the Interim Final Rule.

You may recall that the first appropriation of PPP1 funds was used up in only 10 days, however, an additional allocation of funds was added in late April that still hadn’t been used up by the time the program closed on August 8. In total, over 5.2 million PPP loans were originated totaling over $525 billion, with an average loan amount of $100,729.

It is too soon to tell how quickly the PPP2 allocation will be used up, but there is some good news for small businesses banking with a community bank with less than $10 billion in assets, such as American Riviera Bank! For community and small lenders like us, the SBA will reopen the portal for two days prior to accepting applications from larger and/or online financial institutions.

It appears as though they will also continue setting aside special dedicated hours to process and assist small PPP lenders with their PPP loans, as they did under the second allocation of funds for PPP1. In addition, we understand that there will be a time lapse between the time the lender submits an application and when the SBA approves the loan. This change is to allow for additional compliance checks, and SBA and Treasury Department officials said that lenders should not expect to receive the SBA loan number on the same day the loan application is submitted as we experienced with PP1.

In the Economic Aid Act, Congress has also set aside funds for new and smaller borrowers, for borrowers in low- and moderate-income communities, such as Isla Vista, downtown Santa Barbara, and San Luis Obispo near Old Garden Greek.

These set asides include:

SBA has determined that at least 25 percent of each of those set-asides will go to each one of the groups: loans to borrowers with a maximum of 10 employees and loans less than $250,000 to borrowers in low-or moderate-income neighborhoods.

We are receiving quite a few questions about increases to original loan amounts. The language in the Economic Aid Act, clarified by the IFR, provides for a very specific situation for such an increase where an eligible recipient of a covered loan that returns amounts disbursed or does not accept the full amount for which they were originally approved may be eligible for an increase to their original loan amount. The new rules implementing the Economic Aid Act also provides for two additional scenarios where borrowers can submit requests for an increase to their First Draw PPP loans for partnerships and seasonal businesses. SBA has 17 days from signing of the Act to implement regulations for this provision.

In addition, there are some things to consider. First, the IFR on second draw loans that they may only be made to an eligible borrower that has used, or will use, the full amount of the First Draw PPP Loan on or before the expected date on which the Second Draw PPP Loan is disbursed to the borrower. The IFR clarifies that “the full amount” of the borrower’s First Draw PPP Loan includes the amount of any increase on such First Draw PPP Loan made pursuant to the Economic Aid Act. In addition, the IFR clarifies that the borrower must have spent the full amount of its First Draw PPP Loan on eligible expenses under the PPP rules to be eligible for a Second Draw PPP Loan. SBA believes this clarification will help ensure program integrity by preventing a borrower from receiving a Second Draw PPP Loan if the borrower has not complied with PPP loan program requirements.

You can also refer to the US Chamber for details on other COVID-19 emergency loan programs, including the reopening of the $10,000 EIDL Grant program. Priority for the full amount of the EIDL grant will be given to small businesses with less than 300 employees, located in low-income neighborhoods, who have experienced a 30% reduction in gross receipts during any 8-week period between March 2, and December 31, 2020 compared to a comparable 8-week period before March 2. If you meet this description and received a grant that is less than $10,000 you can reapply to receive the difference.

Previous: Recognizing and Avoiding Scams Next: SBA Accepting First and Second Draw PPP